Feature

Mid point trends: Developments and innovation in food and drink

Plant-based alternatives

Despite some recent setbacks in the alternative proteins market – see the high profile cases of Meatless Farm, Plant & Bean and LoveSeitan all entering administration all in a period of three months – demand is still on the rise for plant-based meat analogues.

Niels E. Hower, new member of the executive board of directors at BENEO and responsible for Meatless – a specialised Dutch company for plant-based texturising solutions – explained that although demand has levelled off, it’s only a temporary hiccup.

“According to latest data [from Forbes and Bloomberg], the global plant-based protein market is expected to reach USD $40.6bn by 2027, with the market for plant-based protein products forecast to achieve a CAGR of 17.57% (2022 – 2027) worldwide,” highlighted Hower.

As the plant-based market gains momentum and customers require higher volumes to meet demand, Hower said many companies are struggling with scalability to achieve mass consumption and price competitiveness in the plant-based category. How fast producers can increase volume will be the make-or-break question.

“A key sticking point for many providers is the need for sophisticated extruders to produce products, that can take one to two years to build,” he continued. “Also, the output per hour of many wet extrusion products is very low and requires a huge amount of fossil fuels.

“To overcome these challenges, Meatless uses standard machinery and, for non-standard production equipment needs, the company collaborates with local partners. Additionally, production can be scaled up quickly, to be more cost efficient and allow the development of more affordable plant-based solutions.”

Manufacturers looking to capitalise on the predicted growth of the plant-based meat alternatives market should be aware of the potential of fish analogues. Fish production is not a problem of efficiency but sufficiency, as a large share of all stock is reaching its limits or has been over fished.

“Plant-based fish alternatives are a relatively untapped opportunity, and this category is being explored by Meatless, with some great product development successes,” Hower added. “For example, substituting the North Pacific pollock and cod is important in the long-term (for fish fingers etc.), given its high consumption.

“With consumers continuing to push the plant-based agenda, the long-term future of the category looks very healthy for those producers who can navigate the challenges of scalability, affordability and new product development.”

With the plant-based meat alternatives trend continuing to provide innovation potential, manufacturers need to conscious of the taste and texture of their products. After all, it has been proven time and again that taste is king for consumers – no matter how sustainable or healthy a product is, your average shopper will turn their nose up if it doesn’t taste good or doesn’t meet expectations.

As Lorna De Leoz, Ph.D. global food segment director at Agilent Technologies, explained, food companies are laser focused on improving the taste and texture of alternative protein products.

“They know if they can achieve a more traditional flavour profile, they can win over consumers at a massive scale – and several recent studies back up this intuition,” said De Leoz.

“The food manufacturers likely to make the most headway will be using advanced chemical analytical technologies to mimic the flavours, aromas and textures of conventional meat products. The next few years will be critical for the industry, and I think we’ll see significant innovations.”

Packaging price trends

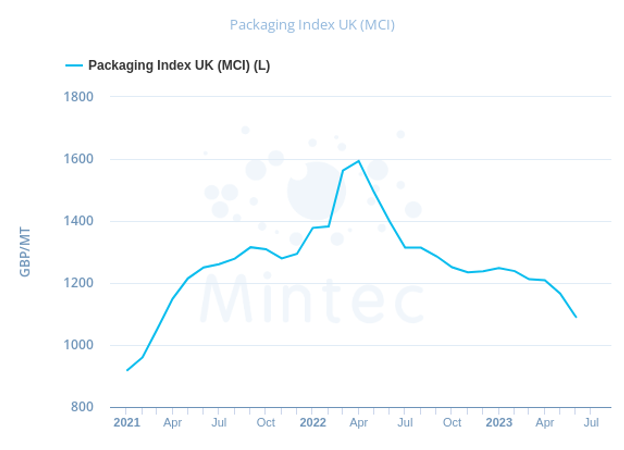

The Mintec Category Index (MCI) UK packaging in June fell by 6.5% month-on-month (m-o-m) and by 22% year-on-year (y-o-y) to £1,090/MT. Full index data for July is not yet available for all products involved in the calculation, but tentatively the index will continue to decline, according to market sources, as plastics and metals prices continued to fall, and only some paper packaging series remained stable.

The main factor behind the decline in prices was the seasonal slowdown in business activity ahead of the holiday season, worsening already weak demand.

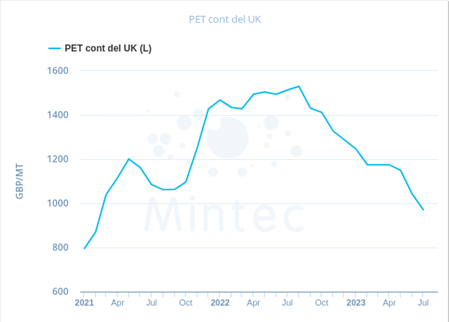

UK polyethylene terephthalate (PET) prices continued to decline for the third consecutive month in July, down 7% m-o-m and 36% at £972/MT. Demand remained weak, the main factor behind the further price decrease.

However, other fundamentals have been driving prices upwards, and many market players think that there is a potential for price rises in the near future. Import pressure on the EU market started to decrease.

Some buyers began to replenish their stocks in July, but this still did not give enough impetus to prices. The cost of PET production also increased, as the contract prices for paraxylene on the EU market rose by €15/MT in June and in July climbed by another €30/MT.

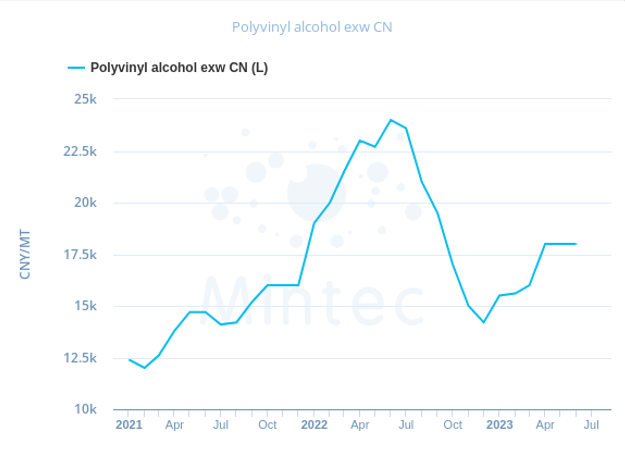

The price of polyvinyl alcohol (PVA) in China has stopped rising since April and remains stable at CNY 18,000/MT. However, market demand remains weak despite China's stimulus measures, and PVA prices are 25% below y-o-y.

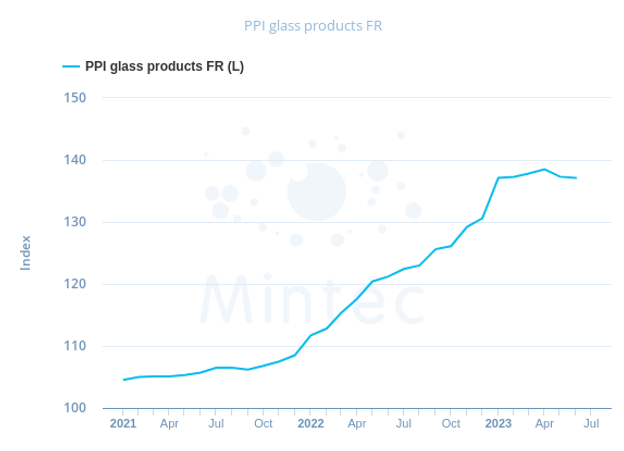

European Producer Price Index of glass products in France declined slightly in May-June but is still 13% higher y-o-y. Glass production, according to the Eurostat index in the EU in May, was 8% lower than in May last year and is declining in line with lower demand.

Sugar replacement

Another trend that sees no sign of stopping is the continued growth of the no and low sugar segment, fuelled by both a swathe of consumers seeking healthier options, as well as legislative restrictions – both current and upcoming – influencing product reformulation.

The combination of evolving consumer preferences and legislative updates has led to an increase in reduced sugar and no added sugar launches, explained Vicky Berry, European business development manager at Synergy Flavours.

“For example, in 2022, we saw a 10.5% increase in soft drink launches with the claim ‘no added sugar’, showing that manufacturers are keen to tap into growing consumer demand for reduced sugar options,” she noted.

Of course, one cannot simply take out the sugar from a product and expect a sweetener to pick up the slack. In one example, Synergy found that reducing sugar in a vanilla cheesecake increased perceived ‘cream taste’ and acidity, but decreased vanilla taste, ‘indulgent mouthfeel’ and sweetness. It’s in these situations that the flavour needs to be built back into the product.

“Some of our solutions work by replicating the taste of sugar, while others aim to balance and harmonise undesirable notes which may come with sweeteners such as stevia or sucralose,” she continued.

“We also support manufacturers in changing their formulations to accommodate rising ingredient costs. Previously, fructose was a popular choice for reduced sugar products, however fructose prices have dramatically increased, so we have supported our customers moving back to sucrose using our taste modulation solutions.”

The move towards reduced sugar content in products has been seen prominently in the soft drinks space, made more pronounced by the sugar levy. But with this switch has also come a greater demand for natural sweeteners – especially in light of the negative press associated with some artificial sweeteners.

“There are notable examples of manufacturers swapping out aspartame, for example Lucozade has made the decision to change to its popular formulation by making the shift to sucralose,” Berry added. “Sweetness from a natural source can also be achieved using stevia in tandem with our taste modulation solutions to deliver desired sweetness, qualifying products for a ‘no artificial sweetener’ claim.

“Taste is usually the top driver for consumers so it’s fundamental that it is not compromised when making formulation changes. This is also essential for bakery applications where sugar, salt and fat play crucial structural roles.

“When reducing these key components in this category of products, sweetness modulators and modifiers used in coordination with our butter flavours and dairy enhancers can help manufacturers to achieve the best quality and taste possible, so a product does not lose appeal.”

Synergy has also witnessed a growth in fortifications and functional additions.

“Energy and alertness was the top active health claim for soft drinks in the UK in 2022, a 12.6% increase on 2021,” said Berry. “Vitamin and mineral fortified beverages and prebiotic launches also increased in 2022.

“It remains important that manufacturers of functional food and beverages consider sugar content as consumers don’t want to negate the benefits of a functional ingredient because of high sugar levels.”

Coffee: More than just the morning brew

The world of coffee roasting has also experienced an increased trend in consumers looking for ingredients the boast health and wellbeing benefits, balanced with the sense of ‘affordable luxury’. Lincoln & York Coffee Roasters category insight manager, Richard Milner, noted more than half of consumers are now making proactive health and wellness choices on a regular basis.

“Traditionally, the reason many of us choose a cup of coffee first thing in the morning as a ‘pick me up’ is the same reason why we might want to avoid it later in the day. With this in mind, we expect decaf coffee to remain in high demand for the rest of 2023,” he explained.

“Advancements in coffee extraction techniques coupled with the growth of speciality coffee have enabled decaf coffee to shake off its reputation of a flat, bitter taste and we are seeing the emergence of some high-quality decaf coffee options.

“Due to these innovations and behavioural changes, out-of-home decaf sales have soared by 11% year-on-year and the out of home decaf market in the UK is now valued at £89m.”

It’s not just your bog-standard cup of Joe that your average consumer is reaching for in the morning either. As Milner tells it, consumers are increasingly trading up for more indulgent offerings such as flavoured coffee.

“The retail market for flavoured coffee is now valued at almost £23m - and we’re seeing flavours such as salted caramel, double chocolate and hazelnut continue to grow in popularity,” Milner continued.

“In terms of flavour preference, we’ve seen a continuing trend towards lighter and medium roast preferences, with these growing by 17% and 11% respectively, while sales of dark roast coffees show continuing decline.”

The popularity for cold coffee has also shown no signs of slowing down, driven by a younger generation thirsty for this growing market – valued at £157.4m this year, up 57% compared to the same period 12 months ago.

“Finally, sustainability also continues to be a key purchasing driver for consumers, especially in coffee,” Milner concluded. “Our research reveals that 63% of consumers are actively looking for sustainably sourced coffee, and that this figure rises as high as 76% in the 18-34 age bracket.

“The same research also reveals that almost half of people are more likely to support brands that are actively reducing their environmental impact, meaning it’s becoming imperative for food and drink manufacturers to build sustainability considerations into their products and operations.”

Wellbeing ingredients on the radar

Nourish Founder Dianna Babics identified some key ingredients in the wellbeing space that should be on manufacturers’ radars.

Medicinal mushrooms

Revered for their stress-relieving, mood boosting and cognition enhancing properties, I’ve been overwhelmed by the explosion of better-for- you products (hot beverages, chocolate bars and snacks) that contain Reishi, Shiitake or Cordyceps mushrooms.

Turmeric

Today, very much part of the health and wellbeing furniture with a good-for-you reputation that harks back to ancient times. Be it tasty shots or energy balls, turmeric continues to build an ardent following among those seeking out its anti-inflammatory, anti-depressant and memory-boosting properties.

Honey

Honey continues to enjoy a real renaissance (sometimes with the addition of CBD) as a sweet treat with raw honey increasingly admired for being a great antioxidant source with peerless anti-bacterial properties. Elsewhere low-carb and ketogenic have not only grown up, but exploded since lockdown as their capacity to tackle both obesity and type 2 diabetes becomes increasingly apparent.

Ready Meals

Perhaps most surprisingly of all has been ready meal’s redemption. Historically pigeonholed as lazy, unhealthy junk food, some brands are now reframing this convenience-led category with unprocessed food heroes made solely from sublime natural ingredients.