The active nutrition market is experiencing dynamic growth, driven by scientific advancements, regulation such as HFSS, and increasing awareness for products that support health, wellness and physical performance.

Speaking with Andreas Petrik, marketing director of specialised nutrition and Paula Limena, vice president for global marketing, health & wellness at ADM, it’s clear that social media has had a huge impact on the health and wellness movement.

Gesturing towards her own wearable technology, Limena said the idea of tracking things such as your sleep, Vo2 max and steps have all become commonplace.

The sports nutrition segment isn’t new, with high protein diets becoming popular among a niche crowd in the 70s and Jane Fonda home workouts following the decade after.

Overview of the sports nutrition market

Today’s approach to sports and ‘being active’, however, is a far-flung cry from the days of the specialist body builder or Lycra-clad instructor on VHS. With the proliferation and versatility of online influencers, healthy eating has been propelled into the mainstream; and food and drink companies have been quick to grab the opportunity which was accelerated by the Covid pandemic.

“The active nutrition market is experiencing notable growth globally and within specific regions like the UK,” ADM said. “According to Euromonitor 2024, the global sports nutrition market is valued at $28.0bn, with a compound annual growth rate (CAGR) of 6% projected between 2023 and 2028. The weight management and wellbeing segment is also significant, valued at $20.9bn globally.”

Growth in sports nutrition has been reflected in high deal volume. Although when compared to the wider industry, the number of larger transactions has been stifled by macroeconomic headwinds, with c.44.0% of deals in the past three years being under £10.0m. according to Oghma Partners’ August 2024 EMEA Sports Nutrition M&A Review.

Recent M&A activity reflects the appetite for sports nutrition, with several notable acquisitions, including Mondelez attaining a significant stake in high protein bar brand Grenade in 2021, Weetabix’s purchase of Lacka Foods (the owner of protein drink brands UFit) in 2022, and Premier Food snapping up FUEL10K just last year.

“Focusing on the UK, the sports nutrition market is particularly strong, valued at $1.8bn and expected to grow at a CAGR of 10.2% from 2023 to 2028. The weight management and wellbeing market in the UK, while smaller at $261m, is still expected to grow at a steady 5.5% CAGR,” continued ADM.

The UK has a young and increasingly health-conscious population, especially those aged between 18-34, at the same time as having a well-established snacking culture. According to ADM, this combination makes it a core market for active nutrition now and in the future.

“Protein and energy shoppers span all age ranges, but their requirements change through the broad generations. For example, Gen Z shoppers are conscious snackers choosing natural sustainable options, and they’re very health & fitness oriented, meaning good nutrition is top of their mind. In general, they are more discerning when choosing their source of protein and energy,” added the experts at UK wholesaler Epicurium.

“Millennials have similar requirements to those of Gen Z, but are more conscious of the functional side of their snacking, meaning they look for protein as fuel for their fitness and fibre for gut health, for example.”

Demand for health brands

The demand for health has also put a renewed focus on labels, with shoppers more keen-eyed than ever before.

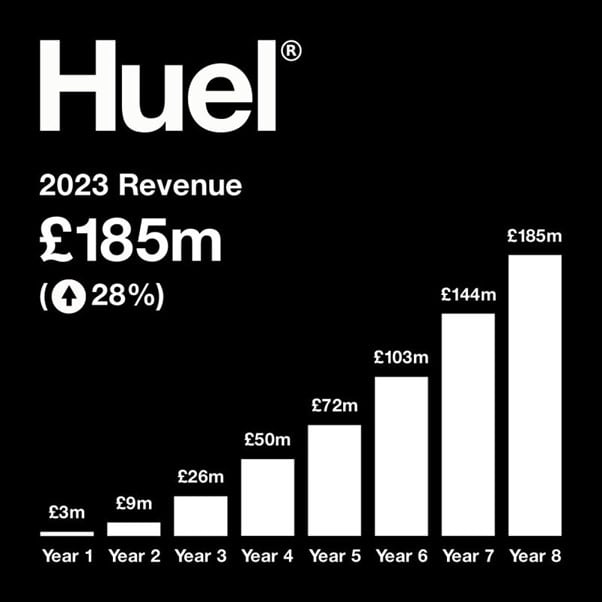

“Consumers today are scrutinising the nutritional profile, ingredients, claims and accreditations more than ever when making purchasing choices. In 2024, according to the Food Standards Agency’s consumer insights tracker, 85% of consumers report they regularly review food labels. This is reflective of a growing awareness around health trends, as well as the anti-ultra processed foods sentiment which remains a contentious, nuanced subject,” explained Dr David Lloyd, senior R&D manager from Huel.

“Specifically, 38% of consumers track their nutritional intake and as such, seek clear information on how products contribute towards their daily intake of macronutrients and micronutrients.”

Since its inception, Lloyd said the meal replacement brand has seen “significant growth”, delivering more than 400m meals worldwide and hitting double digit growth annually.

MyProtein has seen a similar story, growing year-on-year across all areas as it continues to diversify its product offerings, agreeing that today’s market is much more on the ball.

“The customer base is growing and becoming more educated, and therefore knows exactly what they want from their supplements.

“For example, protein supplementation is no longer seen exclusively as a tool to build as much muscle as possible. People understand the long-term benefits of following a high protein diet to live a healthy and balanced lifestyle; something that we continue to build into our brand ethos since our rebrand last year.”

Epicurium also reports an uptick, informing Food Manufacture that the Protein Ball Co., brand’s year-on-year sales have doubled, alongside energy and wellness shots from the likes of Warrior and Xite performing well too.

“High-protein products, often featuring whey, casein, or plant-based proteins like pea and soy, are in high demand,” agreed the team at ADM. “These products are formulated to aid muscle recovery, reduce soreness and enhance muscle synthesis post-exercise. The shift towards plant-based proteins is also notable, driven by both environmental concerns and dietary preferences.”

Gut health

One of the biggest trends permeating the market is gut health, with probiotics, prebiotics, postbiotics all gaining recognition as consumers seek to improve their digestive health, immunity and nutrition.

According to Grand View Research, globally the digestive health products market size was worth $51.62bn last year and it’s expected to grow by 8% in the next 6 years.

“Gut health has emerged as a central focus due to the growing body of evidence demonstrating its critical role in overall well-being,” explained the experts from ADM.

But there is also ongoing research which is examining the wider impact the gut microbiome is having on our bodies, including the aid of lean muscle mass and body composition, as well as mental well-being, which are also prompting new product development.

“Consumers are attracted to products that claim to ‘enhance energy levels’, ‘support athletic performance’, or ‘promote recovery’. These performance-oriented claims make the product more appealing to those seeking functional foods that can help them maintain an active lifestyle,” ADM told Food Manufacture.

Ingredients, flavours and colour

With more and more consumers checking labels and on-going debates around ultra-processing still going strong, the well-known (if still ill-defined) trend of ‘clean label’ will certainly be a concept worth keeping an eye on.

“There is an increasing emphasis on clean label and transparency, with consumers seeking foods formulated with natural, whole ingredients with fewer additives, as well as ethically sourced, non-GMO and organic ingredients just to name a few,” said Lloyd.

On the topic of ingredients, he said ashwagandha, rhodiola, lion’s mane and ginseng have all seen recent favour, as consumers look for products aimed at stress relief and cognitive enhancement.

“Over the past two years, Huel has significantly diversified its portfolio by venturing away from complete meal products,” Lloyd said, citing products such as Huel Daily Greens (comprised of green superfoods, antioxidants, botanicals and adaptogen ingredients) and Daily A-Z Vitamins (a sparkling energy drink fortified with vitamins and minerals).

Based on current trends, Lloyd believes we’ll likely see an expansion into more exotic and functional-associated flavours like yuzu, hibiscus and dragon fruit.

In a similar vein, MyProtein has launched its Green Superfoods, as well as expanding its vitamin line to include gummies and “trending ingredients” such as seamoss, turmeric and ginger.

Epicurium shared comparable sentiments on trending ingredients, adding matcha also to the mix, which in the last few years has been popular in the hot drinks arena.

The UK wholesaler continued: “In terms of flavours, it is those which mimic or replicate classic breakfast moments, for example The Protein Ball Co launching new flavours this year such as Choc Chip Muffin and Coffee Oat Muffin, that are coming to the forefront at the minute.”

Colours have also been playing a role within the active nutrition landscape, ADM added, with certain hues and flavours evoking associations that align with expectations of wellness products.

The ADM team offered orange colours and citrus flavours as a prime example, which have strong links to nature as well as vitamin c and electrolytes, making it a favoured choice in products aimed to support the immune system and maintain hydration.

Meanwhile, green, white and orange colours, paired with flavours such as berries, citrus or tea, are often linked to weight loss and weight management.

“These broad associations are instrumental in guiding consumers' choices, helping them to select products that align with their personal wellness goals,” the ADM experts said.

Moreover, both ADM and Lloyd agreed that hydration products such as electrolyte-enhanced waters and coconut waters are holding firm.

In particular, ADM said ‘rapid hydration’ is taking the sports segment by storm: “These beverages often include electrolytes like sodium, potassium and magnesium to replenish the body's hydration levels quickly and effectively. The rise of recognisable, naturally sourced ingredients, such as botanicals and plant extracts, in these products reflects the broader consumer demand for clean labels.”

On-the-go

Meanwhile, one of Huel's standout offerings has been its Ready-to-Drink (RTD) product, which Lloyd describes as the cornerstone of its retail success. This SKU provides a complete, balanced meal in a convenient bottle format.

“Millions of bottles have been sold every year and the category continues to grow,” added Lloyd.

“This year, we launched our premium ‘Black Edition’ (higher protein, lower carbohydrate) RTD format with 35g of protein per serving and this has been extremely successful in line with the powder equivalent of our product launched a few years prior.”

In terms of format, Lloyd said convenience is key in the healthy food market, which has helped fuel Huel’s RTD uptake, alongside bars and functional snacks as they offer on-the-go solutions for busy individuals.

“Single-serve formats cater to consumers looking for quick, easy options, while in-home multi-serve formats have also appeared recently to be on the rise, providing family convenience without sacrificing quality or nutrition.

“I would expect to see a continued rise in single serve on-the-go formats (beverages, sachets and snacks), and functional products that cater to the demands of busy, health-conscious individuals. As these products become more accessible and offer more added value scientifically, their popularity is poised to grow.”

The future of foods with function

For Lloyd he sees no slowing down for this market’s future.

“The active health food and drink market is, in my opinion, unlikely to deviate from its current trajectory of high growth and innovation; if anything, its growth is expected to accelerate as products continue to improve and health trends become even more mainstream,” he said.

“This is not to say that there won’t be shifts in product formats, ingredients and use of flavours but the overarching macrotrends of health, convenience and sustainability are here to stay.”

The team at MyProtein agreed that whilst the nutrition industry is hard to predict, it’s likely to continue going strong, adding that it could be we see more celebs making their mark in the arena given the success of Prime Hydration.

“If the last 10 years are anything to go by, the market will continue to innovate at a product and brand level.”

Commenting on the future M&A appetite, Mark Lynch, partner at Oghma Partners, added: “Looking forwards, we expect relative valuations to remain healthy and a higher volume of larger deals as economic conditions continue to improve. The prospect of further interest rate cuts will also provide potential buyers notably, private equity with a favourable opportunity to take advantage of this high-growth market.

“The EMEA Sports Nutrition M&A activity has been mainly driven by European buyers representing 88.5%. Over the past 10 years, trade buyers accounted for 78.0% whereas as financial comprised of 22.0%. In terms of targets' location, the UK remains the most prominent region with 35.0% of targets followed by the Netherlands and Sweden.”

In other news, soft drinks manufacturer Britvic has invested £25m into a national distribution centre.