The changing retail landscape has been one of the most significant developments over the past year, as the major high street multiples have lost market share to the limited range discounters Aldi and Lidl.

In an effort to stem the onslaught, supermarkets have started to fight back by cutting their prices and, in the case of some, such as Tesco, sought to reduce the number of stock keeping units (SKUs) they hold. The impact of this on grocery suppliers has been significant, as evidenced by the results of Food Manufacture’s 2015 ‘state-of-the-industry’ survey.

While, overall, 75% of the 511 respondents remain fairly optimistic about the future for their companies (not much changed from 78% in last year’s survey) and for the long-term future of the industry (86% in 2015 compared with 88% in 2014), perennial complaints from suppliers about supermarkets putting the squeeze on them financially; burdensome regulations; and inability to pass on raw material cost increases remain.

A widely held feeling was eloquently summed up by a manager in the frozen foods sector, who complained: “Retailers want to compete with the discounters but still make a larger margin by beating up the manufacturers.” And he added: “Foodservice is in danger of stifling innovation through inertia and commoditisation.”

Another respondent from the frozen foods sector complained: “Raw material price increases and consistent price reduction or rebates to prop up supermarket profits are the biggest challenges.” Complaints about increases in raw material costs were common.

“Manufacturers are being caught between retailers who are looking for price reductions and suppliers who are putting up their raw material costs. It’s a very uncomfortable place to be,” said a technical manager at a snack foods firm.

Looking ahead

Looking ahead commercially, however, life could be set to become a little better. Commenting on the monthly British Retail Consortium (BRC)-KPMG Retail Sales Monitor for May last month, City analysts Clive Black and Darren Shirley from Shore Capital noted that food was at last starting to show some positive signs.

“We see an industry that continues to go through the structural change of the major superstore groups seeking to regain customer trust and support,” said Black and Shirley. “Hence, alongside soft commodity markets, particularly for sugar, potatoes and dairy products, we also see self-imposed dis-inflation and gross margin investment.”

They added: “What is particularly welcome for the domestic food chain, though, is the return of positive volumes, partly a function of favourable multi-year comparatives and partly a result of those lower prices. Additionally, therefore, it is pleasing to see positive overall food sales in the BRC-KPMG survey.”

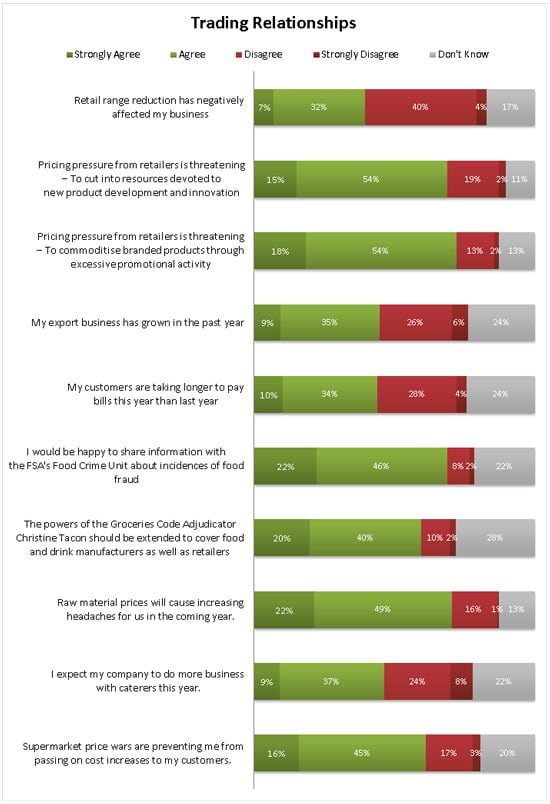

Food Manufacture’s survey shows that 75% of respondents expect their firm’s profit margins to improve over the coming year, slightly up on the 72% that expressed this view last year, while 73% expect consumer spending to rise over the coming year, compared with 75% last year. Meanwhile, the impact of retailers reducing their SKU numbers does not appear to have fed through to most suppliers yet, given that just 39% reported that retail range reduction had hit their businesses.

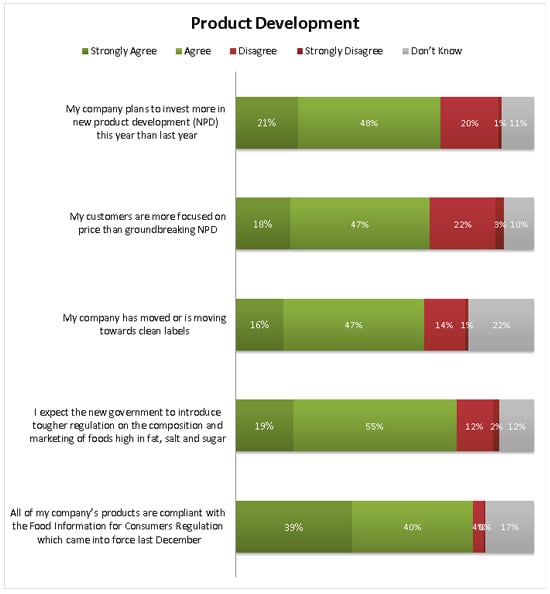

The importance of new product development (NPD) continues to be widely recognised in the sector, with 69% (66% last year) of respondents planning to invest more this year than last year. However, most people (74%) expect tougher regulations to be introduced on the industry governing the composition and marketing of foods high in fat, salt and sugar. Respondents also report that pricing pressure from retailers continues to hit NPD (69%), albeit at a slightly lower level than last year (72%). Pricing pressure from retailers for promotions also continues to threaten to commoditise branded products (72% compared with 75% last year).

Earlier this year the Groceries Code Adjudicator Christine Tacon announced she was to investigate claims that Tesco had treated its suppliers unfairly under the Groceries Supply Code of Practice. She expressed “reasonable suspicion” that Tesco had breached the code.

But Tesco is unlikely to be the only retail culprit. Although not named, one respondent complained of a continuing problem of “deductions from one customer after orders had been delivered in-full and on-time”.

It was also interesting that 60% of survey respondents agreed that Tacon’s powers should be extended to cover food and drink manufacturers’ treatment of their suppliers as well as those of retailers. While Premier Foods was last year accused of treating some of its suppliers badly, these findings suggest that other food and drink manufacturers are also guilty of adopting dodgy practices for their suppliers.

One contractor complained: “Food factories are extending the payment terms and insisting on prohibitive ‘retainers’, which hugely affects my company’s cash-flow.”

Following the establishment of the Food Standards Agency’s (FSA’s) Food Crime Unit (FCU) last December in the wake of the 2013 horsemeat scandal and the subsequent Elliott report, 68% of respondents said they would be prepared to share information with the FCU about incidences of food fraud. This is surprising, given that many in the food industry have expressed concerns in the past about sharing sensitive information with the authorities for fear it might be used against them.

Guilty until proven innocent

“The FSA in my sector treats food business operators as criminals: guilty until proven innocent!” complained one quality assurance manager in the meat sector. “There is no working together to achieve the common goal of high quality meat that is safe and cost effective. The motto used to be ‘what can we do to help?’; nowadays it is ‘we’re coming for you’.”

Meanwhile, the strength of the pound and the eurozone crisis appear to have hit exports of food and drink, with just 44% claiming their export business had grown over the past year. It is interesting to compare this figure with the 62% that last year said they were keen to explore exports over the coming year.

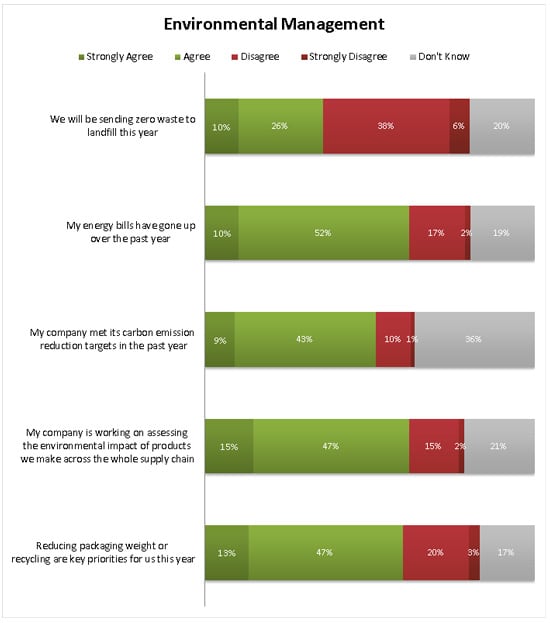

As far as environmental management is concerned, it is clear that the industry still has much more to do, with just over one-third (36%) hitting the 2015 target set by the Food and Drink Federation of sending zero waste to landfill. More positively, 62% are taking a more holistic approach to product lifecycle management and setting out plans to assess the environmental impact of products across the whole supply chain. A total of 60% are also planning to reduce their packaging weight or intend to make recycling a priority this year.

Following the introduction of the Food Information for Consumers Regulation last December, the vast majority (79%) of respondents claimed that all their company's products were now compliant.

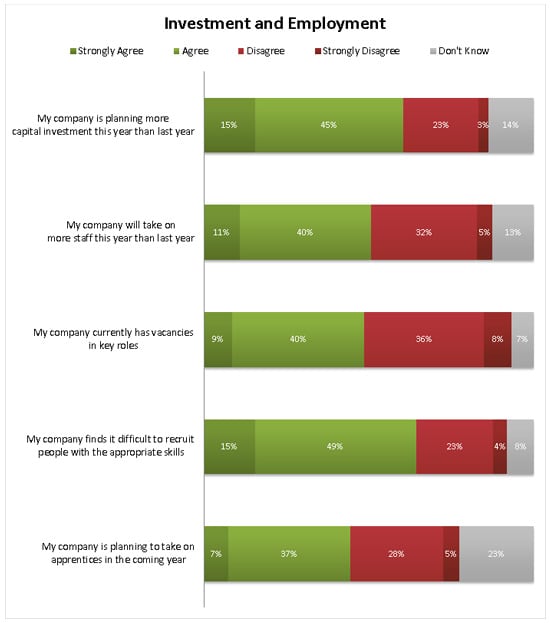

While responses to questions about investment and employment plans were remarkably similar to last year, a new question this year about their company’s plans to take on more apprentices over the coming year saw 44% of respondents agreeing. With the impending skills crisis, it might be thought that more needs to be done in the area of training.

Lastly, given the importance of the EU to the food and drink sector – both regarding legislation and as a trading partner – it is surprising that very few (three) respondents mentioned any concerns about a possible UK exit (Brexit) following a referendum on membership before the end of 2017. Maybe a question on the subject in next year’s survey, when the full implications of a Brexit become evident, would elicit a bigger response.